How to Save $20,000 per Year With $54,000 Salary

Colleges don’t teach how to save boat loads of money. But, who does?

Where can you learn about saving money and personal finance?

Is there a one size fits all solution that you can use save money?

Answer is yes and no.

There are so many ways to save money.

- Smart Ways – Have a plan and target and work to reach your target. Plus, get educated about personal finance.

- Frugal Ways – Extreme ways that others will frown upon.

- On The Go Ways – I don’t have a plan, but I limit my spending

- Hybrid Ways – Mix of smart and frugal ans On the Go.

- I Don’t Care Ways – All this stuff id way above my head. Just give the Dang Salary, Will ya?

Today, I’m going to share an experience posted in the comment section of how much money can you earn and save in H1B and L1 Visa.

This person is saving over $20,000 per year.

How to Save $20,000 per year

I am a recent grad from a masters program (non-tech) and currently earn $54,000 per year.

I also live in Washington DC which is extremely expensive. I pay $1500 for a studio that I share with my boy friend. Despite this, there is no reason why I can’t save 20,000 and more annually.

How do I do this?

Living in Washington DC means I don’t need a car and transport is not too expensive (under $100 per month).

We cook a lot, we go out with friends often for happy hours but while they may down 5-7 drinks we stick to buying 1-2 beers to keep spending down.

We don’t dine at fancy places instead we spend money on traveling and visiting new places (and that is a priority for us, but everyone has different priorities).

My employer matches my 401k upto 4% gross which vests immediately, so that’s 4.5k between both of our contributions.

I started a Target Retirement Roth IRA with Vanguard (if you want to invest in stock market long-term but do so passively, a Roth IRA is your best bet!).

I put in the maximum annual allowance or $5.5k – so I’m at 10k savings with that.

I also set aside $1000-1200 from my paycheck into a separate online savings account.

Plus I expect to get $1-1.5k back in tax refunds during the year.

So I’m already at $25k annual savings not including any investment gains (or losses) during the year.

It is totally doable without being a “stingy” Indian. And oh yeah, I didn’t have any student debt at graduation (no my parents didn’t pay for it – I worked 2 jobs + scholarship) nor am I stupid enough to rake up any credit card debt (that’s for irresponsible American kids).

And no I do not plan on going back to India every year or “buy expected gifts” for relatives (Do Not build such expectations).

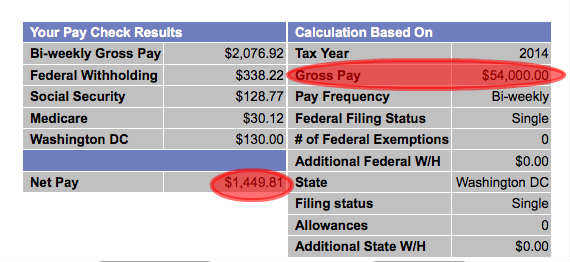

Sample Bi-Weekly Pay for $54,000 Salary

Now, you know a way to save $20,000 per year. Can everyone save that kind of money or even more than $20,000 per year?

Here’s Sample Bi-Weekly Pay Check for $54,000 per year salary (without taking any state tax deductions) from Adp Pay Check Calculator.

When your salary is $54,000 per year, you can expect to take home around $1449 bi-weekly. I’m showing this as an example of what to expect as your take home pay and how much you should plan to save per pay check to meet your targeted savings.

Related : Sample Pay Stub and Payroll Taxes Explained

Yes, it is absolutely possible to save $20,000 per year provided you earn enough salary. But, You have to be smart, get yourself educated about personal finance, money, savings and investing, then create a plan and follow the plan.

In above example, here’s the plan

- Don’t spend on dinning out

- Save for Travel

- Automated Savings per month

- Invest in 401k

- Invest in Roth IRA

That’s a simple 5 step plan. Easy to Follow and Step 2 to 5 can be automated with direct deposits to bank accounts from the pay check.

How to Save $1666 per month

To Save $20,000 per year, you have to save $1666 per month.

If that’s your target then go out and learn how to save $1666 per month. Once you figure out the ways to save money and cut your expenses without torturing yourself, you can put your savings on auto pilot by scheduling direct deposits, setting up automatic bill pays.

Everyone approaches saving money in a different way. But, most common theme is “Don’t spend to save money”.

Here’s how I approach personal finance and saving money : Earn more to save more.

Why?

There’s going to be an upper limit on how much you can save with your fixed income.

Lets say, you earn $50,000 per year. If you want to save $20,000 per year, you create a plan to do that.

But, to save an extra $2000 per year from the same income, you have to be really frugal and do extreme things.

You will be probably investing more time than what’s your time is worth. Like spending two hours to find a coupon to save $2.

When that two hours of your time is worth say $12, does it make sense to spend $12 to save $2?

But, if you invest same two hours to earn more money, you increase the upper limit without sacrificing your way of life.

How about creating a passive income stream?

- 22 Different Ways to Make Money by Blogging

- Maybe Investing in Stocks

- Freelancing

- Convert your hobby to business

Summary :

Now, you know how one person is saving $20,000 per year ( almost 50% of the salary ). Plus, my approach towards saving money.

Remember this, your priority and needs to save money will be different from others. There’s no one size fits all solution. But, having a plan is better than not having one. First it start with getting educated about personal finance. No body teaches you this kind of stuffs in college. You have to grind it out and create a plan to earn and save more money.

- What is your approach towards saving money.

- Do you have a plan?

- Can you share the plan with us?

If you were saving in your 401k why is that not in your paycheck calculator

Pretty bold and immensely ignorant to assume that everyone who has credit card debt is stupid. Debt is symptom of a much larger problem in this country – inequality is the larger issue and it stems from attitudes like yours. Access to healthcare, college, and housing is a real issue for many Americans who feel like that have NO CHOICE. Most people aren’t just buying sh*t. They’re trying to live.

“That’s for irresponsible American kids” ….this article is a joke. YOU do not save $20k a year, you and your boyfriend save $20k a year.

I am 23 years old. Graduated with out debt. Earned around $54,000 the first year of my career and put in $17,000 in my savings account from that total. I am single and choose to live with my parents. Pay them $500 monthly. My mother and I take turns cooking so I don’t eat out much. When I do eat out, I use coupons the restaurants send in the mail (I don’t mind paying regular price if no coupons are offered). I rarely pay for things at regular price so, you will see me in the clearance section buying clothes or buying groceries that are on sale. And I only buy fruits and vegetables at a farmer’s market. I pay almost everything using my credit card to get a lot back in rewards to put in my checking account. My credit card statement mostly consists of food and gas. The only thing I truely splurge on are video games, but I am able to have a fair amount of self control.

“Oh, by the way I don’t have any college loans” he mentions at the bottom of the article. Yeah, no shit. It would be EASY to save $20K if I wasn’t contributing $1K a month to student loans.

Unless you are paying half of all household expenses like rent, insurance,utilities ,medical insurance you are not saving 20000 out of your 54000, you are saving 20000 out of two jobs (one paying 54000 and the other involves being a girlfriend to someone who pays you money indirectly). And if your target is really saving money the first 54000 job is not that great. The other one can be much more paying especially if you get multiple clients willing to pay 100 dollar plus for 30 mins.

from you calculation saving 1666 every month only leaves you about 1230 in disposable income. your rent alone would wipe out that 1230. I assume saving the 20K per year depends on being in a dual income household.

Most of these articles make it seem like it’s one person saving a certain amount per year, but it’s actually one person saving that amount while their SO pays for the bills. It’s not really helpful for single people.