4 Options to Pay US University Tuition Fees

Once, your F1 Visa is approved, you are going to start thinking the folowing.

How to Pay the College Tution Fees?

How to take the money with you for Living Expense?

Which option gives the best Foreign Exchange Rate?

If you have a student loan, bank manager might add few more wrinkles to this process.

Let’s dig deeper about money transfer options.

List of Options to Transfer Money to the USA

- Demand Draft (or Cashiers Check)

- International Wire Transfer

- Direct to Your Bank Account

- Direct to Universities Bank Account

- Using FlyWire

- Foreign Exchange Travel Card

- Travelers Check

Do the bank (in India) actually give the amount directly to the US? Also, if we pay the university, they won’t give us our livelihood expenses and insurance out of it? So, please advise.

Vijay

1. Pay via Demand Draft (or Cashier Check)

Students from India will know this option – Demand Draft. In other words, you can call it as Cashiers Check.

Demand Draft (DD) is issued to a specific Business or a Person.

- Get Demand Draft from Bank in India for certain amount greater than estimated tuition fee

- Sometimes Banks will give DD only in the university as a single draft

Example – First-semester Tuition fee – $9,000. You can get DD for $10,000 (payable to the University).

Pay the fee using the DD ($9,000).

Your University will process the fees.

Let’s say it comes to $9000 (Including Insurance). Remaining $500 will be credited back to you.

Typically university will send a personal check to your name.

You can deposit that check into your bank account (in the US).

This whole process takes about 20 to 30 days.

Some Universities charge an additional fee for processing the Demand Draft. Check with your university’s payment options.

2. International Wire Transfer

Several students take this route by using International Wire Transfer to make the Payment.

- Direct Transfer to University Account

- Transfer to Personal Account to University Account

In general, banks in India will not allow Wire Transfer direct to students account if the money is part of an approved Education Loan.

2.1 Direct Transfer to Your Account & Pay With Credit Card

If the money is coming from your savings or parents savings account, then you have an option to send the money to your Checking Account and then pay the University using your Credit Card (if you can) or via Check.

If the University gives an option to Pay via Credit Card and if you meet the following conditions, then consider making the payment via Credit Card.

- Credit Card gives you Points

- You have a new card and need to meet the Spending Requirements

- There’s no Fee for Paying using the Card

- You will break even if university charges transaction fee (by points)

Additional Processing Fee could make this transaction expensive.

Here’s the Payment option from UNC-Chapel Hill. It has a 2.85% processing fee.

Here’s another example from the University of Texas at Arlington about additional fees of 2.25% for paying via Credit Card.

If you are going to pay $10,000 in Tuition fee, 2.85% will add an additional $285 to your bill.

I have seen friend use the Credit Card to make the Fee in UT Arlington, when they did not have the money to pay the fees.

2.2 Direct Transfer to Your Account & Pay With Personal Check

If you received money as Direct Transfer into your Account, then you can pay the Tuition fee via Personal Check.

For Check from Domestic U.S. Based Banks, there shouldn’t be any processing fee.

If you are have savings from your part-time job, internship or assistantship, you would use Check to Pay the fees.

2.3. Pay via FlyWire

Several Universities are now offering an option for International Students to pay the University via Flywire.

This option will allow your parents to send the money in the local bank in your home country to FlyWire and they will transfer the money to Universities account.

Here’s an example from the University of Texas at Arlington.

3. Pay Using Forex Travel Card

Paying using Forex Travel Card is also a popular option.

If University is not offering Flywire option, and for some families, if Wire Transfer is not a possibility, then Forex Card might be the way to go.

As you can see the Processing Fee and the exchange rate can differ a bit based on the companies that issue the Travel Card.

4. Travelers Check

I’m not sure if anyone uses Travelers Check these days.

Amex Travelers Check is as good as Cash.

Anyone in the possession of it can cash it. I would not recommend this option.

Even if you were gives this as an option, please stay away.

If you happen to lose this Amex Travelers Check, you will be trying to find ways to salvage the funds.

I don’t Recommend Carrying Thousands of Dollars as Travelers Check to pay your college tuition fee.

Summary: How to Pay Tuition Fee

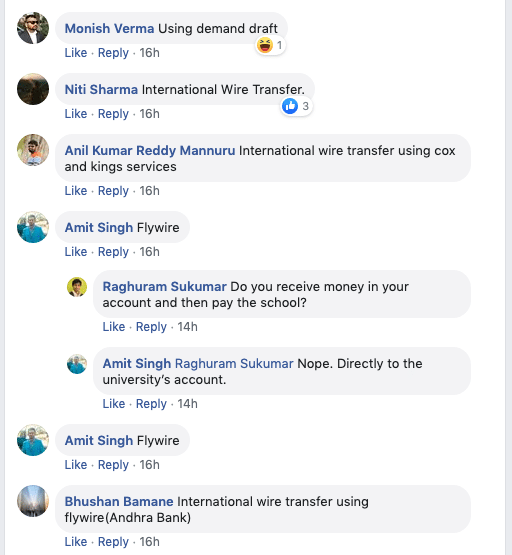

I posted this question to a wider audience in the F1 Visa Facebook Group.

Here’s the response from several members.

I think the above screenshots sums-up the different ways F1 Students are paying their tuition fees.

Pick one that you will comfortable and that gives the best bang for your buck.

Related Articles in College Tuition Fees

- Difference Between In-State vs Out of state Fees for International Students

- How to Calculate Total Tuition Fees from the Form I-20

- What is Credit Hour, Duration of Degree and Tuition Fee?

- How to Pay the Tuition Fees to the College – 4 Options (this article)

- Total Cost of Studying Masters (MS) Degree in the USA

i need $400 to pay tuition fees for college, I have applied for a fafsa loan for full time tuition. but i need to pay this additional amount. that is not covered by fafsa. it is from last year. and fafsa onlt covers the current year. this will allow me to register for part 2 of fall semester. i am majoring in accounting. and I really need the money

ASAP. thank you.

Hello Every Body!!!

First of all, thanks to all for nice and ur important blogs which helps for new a lot.

I am new here I want to do GRE but I dont have Idea that which Book will be good for preparing, and what is requirement to give examination.

I have economy problem to study in foreign and how i can take loan for this….

Thanks in advance…..

Please provide guidance on working when we study in US…. Please do share which might be a very useful one……… thanks in advance….

thanks prashant, it will be helpful for me.

I took my educational loan Credila and right now I am in CU-Boulder… I have had a great experience with Credila till now… They sanctioned me 20 lakhs for the whole course (remember Credila funds more than 20L too unlike other Govt Banks…) They asked me how much money is required for the first semester, I had asked them certain amount for the Fees (to the univ) and some for my Living expense… Even the mode of transfer was the one i chose… I asked them to Wire transfer the fees to the Univ (the univ told me that Wire Transfer is their preferred method) and for my living expense, I had asked 1000$ in Forex Card and 2000$ in TC, which they did without any hassles… I just visited their office in Chennai twice… Once to sign the agreement and the next time for collecting the TC and the Forex Card… They approved the loan without my i20, without me visiting the bank even once and they sent me the Sanction letter in Courier… When hearing about these hassles which the fellow students face in govt banks, I think its time for the Govt banks to wake to the Private players…

As it is the case with every other thing in this world, Credila too has some Cons… They are… Their interest rate is A BIT high… They offered me 12.95%… which is the highest they offer… depending upon the collateral you provide they reduce it further… As in my case, the collateral i provided to them was already under mortgage at HDFC (their parent company)… But still I think only a couple of banks offer interest rates which are lower than 12.95%… and the other thing is that, My parents need to pay the interest while i am actually studying here… Its not like some govt banks like SBI where you can waive off to pay the interest while you study… But still credila had an option for me… I can choose the % of the total interest i can pay them while i study… I chose to pay them 25% (which is the minimum) of the total 12.95%…

WHY I WENT FOR CREDILA inspite of these Cons is that: Only Credila sanctions a Loan without a i20… I used my Sanction letter from Credila and showed CU-Boulder that I have enough funds for my studies (which i need to prove to any univ to get i20 from them) to get my i20… And the collateral i had planned for my Educational Loan was already under Mortgage at HDFC…

So I dont regret taking Loan from Credila despite reading many negative reviews about them online, but I thank them each time when i come across posts like these, for the hassle free loan they offered me and I am here now in USA pursuing my Dream..!

Hi,

Thanks for the post! I was looking for some reviews for Credila and to be honest, I found more negative ones than positive. Glad to hear that your experience with them has been good.

I am planning to apply for a loan with Credila. How long do they take to give the sanction? Also, is it okay if my parent and I live in different cities and the collateral property is in the same city as my parent?

Thanks for your time!

Also, I forgot to add one more point. Recently, in Kerala they have implemented a rule such that if one is applying to an educational loan, he should go and seek only the bank which is allotted for his ward(residence). Every bank has been allotted so and so wards, and so that appropriate loan aspirants must approach only the assigned bank. I don’t know if this is implemented throughout India. This may also depends upon the bank manager. he has sole powers. (And mostly if your banker is impressed with your accounts or your parents account, he might not hesitate to grand you the loan no matter what ward you are in 🙂 ). Thanks again for the help HSB.

The above said rule was told to me when i applied for loan in Madurai, Tamil Nadu. I gave a written request to the Collector he then forwarded the application to the bank.

good one

Thanks for the resource HSB. You understood my query even though I mis-explained. I think I have to educate the Bank Manager or try a new bank :).